Metallurgical accounting consulting: AMIRA P754 audits & system design

Metallurgical accounting is the bridge between your technical operations and financial reporting. It transforms process data into trusted production figures reliable enough for operational decisions, auditable enough for stock exchange disclosure.

Many operations struggle with metal balances that won’t close, systems that fall short of AMIRA P754 requirements, or data quality gaps that create regulatory exposure. These are not just technical problems. They are financial risks. How large? In one CASPEO audit, a 0.29% slag‑sampling bias cost a copper smelter USD 9.54 million per year, even though the site’s metal accounting system still appeared “balanced.”

CASPEO is an independent consulting firm delivering metallurgical accounting services built on AMIRA P754 code, Pierre Gy’s Theory Of Sampling, and advanced data reconciliation methodologies. With 20+ years of experience, we help miners turn operational data into compliant, auditable metal balances through expert audits and implementations.

Why metallurgical accounting matters

Metallurgical accounting is the process used in mining and mineral processing to measure, track, and reconcile metal flows from ore feed through processing to final product. It provides a quantified view of plant performance, process losses, and inventory levels shared by operations, finance, and management.

It sits at the interface between technical and financial performance measurement. Production data generated to manage process performance is used to value products and inventories in financial accounts (Brochot & Durance, 2012, 11th Mill Operators’ Conference).

Metallurgical accounting depends on three technical disciplines:

- Representative sampling (data quality at source)

- Data reconciliation (statistical coherence of mass balances)

- QA/QC procedures (auditability of the measurement chain).

When any component fails, the consequences are financial:

- Undetected production losses: measurement biases hide real metal flows; phantom inventory accumulates in WIP accounts

- Commercial disadvantage: in concentrate trading or offtake agreements, the party with more accurate measurement data negotiates from a stronger position

- Regulatory exposure: NI 43-101, JORC, SOX, and GISTM all require auditable metal balance documentation; gaps create simultaneous disclosure risk across frameworks

Metallurgical accounting in today’s regulatory landscape

Regulatory scrutiny is rising across financial reporting, mineral reserves disclosure, and supply‑chain transparency. AMIRA P754 is the technical framework that ensures compliance with these wider requirements. A weakness in the metal accounting system creates gaps across all of them.

Today, stock exchanges and reporting bodies increasingly reference P754 as the production reporting standard. A metal accounting system built to AMIRA P754 provides the level of control, traceability, and auditability required to meet the production‑data expectations of SOX, NI 43‑101, JORC, SAMREC, and GISTM.

AMIRA P754: the foundation

Published in 2005, the AMIRA P754 code of practice established a framework to track metals through the entire mining value chain, from ore extraction through processing, smelting, refining, and final product.

It defines 10 principles for best practice metallurgical accounting covering accurate measurement, transparency, audits, data verification, and governance. But AMIRA P754 didn’t emerge in isolation. It developed alongside broader corporate governance reforms following early 2000s financial scandals.

Today’s converging regulatory frameworks

Modern metallurgical accounting now sits at the intersection of multiple regulatory requirements:

- Corporate governance: Sarbanes-Oxley Act (SOX), Combined Code (UK), King III (South Africa)

- Supply chain transparency: EU Critical Raw Materials Act (CRMA), Conflict Minerals Regulations

- Environmental management: GISTM tailings standards, environmental reporting, closure planning

- Stock exchange standards: NI 43-101 (Canada), JORC Code (Australasia), SAMREC (South Africa)

CASPEO’s metal accounting consulting expertise

CASPEO’s services cover the full lifecycle of a metal accounting system: diagnosing what is failing, building what is needed, and aligning procedures with AMIRA P754. All services are independent of software vendors, equipment manufacturers, and laboratory providers.

Our advisory services replace fragile spreadsheets with robust workflows and align governance, reporting, and procedures. The result is a transparent, compliant system aligned with AMIRA P754 and industry best practices that supports confident operational and financial decisions.

Explore our metallurgical accounting services:

- Metal accounting audit of existing systems

- Set up or revamp of metal accounting systems

- Alignment with AMIRA P754 code of practice for metal accounting

Regular compliance audit

Metal accounting audit of existing systems

CASPEO conducts in-depth audits of existing production and inventory metallurgical processes to evaluate their compliance with AMIRA P754’s principes, and identify technical deficiencies compromising accuracy, transparency, or auditability.

The audit examines the full data chain across five domains:

- Sampling and mass measurement: protocols, equipment geometry, calibration, measurement uncertainty

- Metal balance calculations: reconciliation methods, treatment of biases, inventory handling

- Data management and reporting: sources (SCADA, LIMS, historians), traceability, manual interventions

- QA/QC documentation: procedures, control charts, audit trails, non-conformance handling

- Governance structure: documented roles, approval workflows, internal and external audit procedures

The audit covers the sampling layer explicitly because metal accounting accuracy depends entirely on measurement quality at source. This is where most undetected losses originate. CASPEO uses a seven-domain measurement system audit framework and the uncertainty budget method (OE = TE + AE) as the quantitative basis for all recommendations (Brochot, 2015, TOS Forum, DOI: 10.1255/tosf.73).

This service is an integral part of any metallurgical accounting system implementation or revamp project, and can also be delivered as a standalone engagement.

THE RESULT

A comprehensive understanding of system compliance with AMIRA P754 principles, quantified measurement uncertainty budgets, and a prioritized roadmap for improvement, highlighting quick wins and longer-term actions to enhance reliability and transparency.

Metallurgical systems implementation

Metal accounting system design and implementation

CASPEO designs and implements integrated metal accounting systems that centralize data from multiple sources (Historian, SCADA, LIMS, ERP), apply rigorous reconciliation logic, and generate auditable metallurgical balances aligned with AMIRA P754.

The implementation follows a structured six-step methodology:

1. Diagnostic assessment: review of measurement systems, data flows, reconciliation methods, and governance structure

2. System design: mass balance boundaries, inventory points, accuracy targets, and governance framework aligned with AMIRA P754

3. Measurement and uncertainty definition: documented sampling procedures, assay protocols, and quantified measurement uncertainties for all critical streams

4. Software configuration and integration: INVENTEO configured to collect data from existing sources with transparent reconciliation logic and automated reporting

5. Testing and validation: parallel calculation runs, balance verification, reconciliation performance testing

6. Training and governance rollout: cross-functional training (metallurgy, production, finance); formalized roles, approval workflows, and audit procedures

This structured lifecycle approach (implementation, production, closing phases) was first described in Brochot & Durance, 2012. The application of sampling theory within the INVENTEO methodology connecting measurement uncertainty directly to reconciliation accuracy is documented in Brochot, 2011, 5th World Conference on Sampling and Blending.

Powered by INVENTEO, CASPEO’s metal accounting software, your system becomes a trusted source of truth, delivering reproducible results that stakeholders across your organization can rely on.

THE RESULT

An integrated automated metal accounting system compliant with AMIRA P754 that reduces financial risk, meets the highest governance standards, and scales with your operation. It also provides a reliable foundation for performance analysis, inventory control, and ongoing operational improvement.

Compliance gap analysis

Alignment with AMIRA P754 code of practice for metal accounting

For operations still running metal accounting in Excel or with in-house tools that cannot meet AMIRA P754 requirements, CASPEO performs a structured gap analysis and defines a phased implementation roadmap.

Our metal accounting consulting review ensures your procedures align with the 10 principles of AMIRA P754, including:

- Measurement accuracy targets for flows and assays (Principles 1, 2)

- Transparent calculation rules and single-direction information flow (Principle 3)

- Competent person oversight and documented responsibilities (Principle 4)

- Data validation and reconciliation to guarantee consistency (Principle 5)

- Routine internal and external audits (Principle 6)

- Governance, reporting workflows, and accountability structures (Principles 7–10)

Spreadsheets cannot satisfy AMIRA P754 Principle 3 (immutable audit trail), Principle 4 (competent person controls), or Principle 5 (automated data validation) at scale. Where needed, we support transition to INVENTEO, CASPEO’s proprietary metallurgical solution which embeds agreed procedures, automates calculations, and improves traceability.

THE RESULT

A revised metallurgical accounting methodology, updated operating procedures and work instructions, and an audit‑ready documentation set that shows how the site applies AMIRA P754 in practice. Includes a phased implementation roadmap prioritized by impact.

What a compliant metal accounting system delivers

Operational visibility

Continuous, reconciled view of metal flows, recovery performance, and process losses across the full value chain

Audit readiness

Traceable, documented data chain with immutable audit trails that CFOs, external auditors, and regulators can verify

Financial risk reduction

Biases that translate to millions in undetected losses or commercial disadvantage are identified and corrected

Reduced manual effort

Automated data collection, reconciliation, and reporting replace spreadsheet workflows

Regulatory compliance

AMIRA P754 simultaneously satisfies SOX, NI 43-101, JORC, SAMREC, GISTM, and supply chain transparency mandates

Scalable governance

A system designed once scales with new streams, commodities, and regulatory requirements

Why CASPEO for metallurgical accounting and reconciliation consulting

Independent expertise, proven over 20+ years

CASPEO provides independent metal accounting consulting free from manufacturing or lab system vendor affiliations.

Recognized experts in AMIRA P754

CASPEO is an industry‑recognized AMIRA P754 authority with documented, real‑world expertise.

Operational excellence focus

CASPEO designs production accounting systems serving both regulatory compliance and operational improvement.

End‑to‑end metal accounting

CASPEO supports metal accounting across concentrators, smelters, and refineries, tailored to each commodity.

Expertise from sampling to reconciliation

CASPEO covers every layer of metallurgical accounting, delivering integrated solutions rather than isolated fixes.

Knowledge transfer and training

Every implementation includes training so your team can operate, maintain, and adapt the system independently.

More than consulting, a fully integrated approach to metal accounting

CASPEO offers a unique approach to metallurgical accounting by combining expert consulting with advanced software to deliver reliable, AMIRA P754–aligned systems. We support operations with audits, system design, implementation, and training because accuracy and compliance depend on people, processes, and tools working together. Most sites choose our integrated model: consulting, training and INVENTEO automation.

CASPEO unites consulting, software and training for true metal accounting

Consulting

Full on-site plant audits, AMIRA P754 compliance roadmaps, documented system, implementation support

INVENTEO software

Automated data management and reconciliation, metal balance, audit-ready reporting

Courses

Self-paced courses on metal accounting and principles, on-site workshops, ongoing knowledge transfer

+

CASPEO masters all pillars of metallurgical accounting

Stéphane Brochot: metallurgical accounting expert

Stéphane Brochot is Co-Manager at CASPEO and an active member of the International Pierre Gy Sampling Association (IPGSA). His research on metallurgical accounting methodology, measurement uncertainty, and the financial consequences of sampling bias is published in peer-reviewed journals and major international mining conference proceedings.

Selected publications on metallurgical accounting and metal balance reconciliation:

- Brochot, S. (2015). The overall measurement error – TOS and uncertainty budget in metal accounting. TOS forum, 2015(5), 83-86. DOI: 10.1255/tosf.73

- Brochot, S. (2021). Metal accounting: a direct link between sampling and financial management. Spectroscopy Europe, vol. 33, no. 7.

- Brochot, S. & Durance, M.-V. (2012). A New Approach to Metallurgical Accounting. 11th Mill Operators’ Conference, Hobart, Australia, pp. 217-223.

- Brochot, S. (2011). The application of sampling theory in the metal accounting process – INVENTEO methodology implementation. 5th World Conference on Sampling and Blending, Santiago, Chile, pp. 185-193.

- Cappai, L., Gonzalez Fernandez, M., Brochot, S. & Vix, P. (2016). Metal Accounting: The Core Responsibility of Process Engineers. Procemin 2016, Santiago, Chile, Chapter 3, pp. 1-14.

Engaging CASPEO on metallurgical accounting and reconciliation means direct access to Stéphane Brochot’s technical knowledge and field experience across mineral commodities and processing environments.

Frequently Asked Questions (FAQs) on metallurgical accounting consulting services

What is metallurgical accounting?

Metallurgical accounting is the process used in mining and mineral processing to measure, track, and reconcile metal flows from ore feed through processing to final product. It quantifies metal recovery, identifies process losses, and produces auditable production figures for operational management and financial reporting.

A metallurgical accounting system combines three components:

- Representative sampling and measurement at each process point

- Data reconciliation by mass balance for statistically coherent metal balances

- Governance and reporting procedures aligned with industry standards such as AMIRA P754

▶️ This article could interest you

The AMIRA code principles and how to implement them

What is the financial risk of unreliable metallurgical accounting?

Unreliable metallurgical accounting creates three categories of financial risk: undetected production losses, commercial disadvantage in concentrate trading, and regulatory exposure across multiple frameworks.

In a documented case, a copper smelter with a 0.29 percentage-point slag sampling bias was losing USD 9.54 million per year while its accounts reported a balanced ledger. In concentrate trading, a 0.175-point Cu grade discrepancy on a 17,000-tonne delivery amounts to ~$280,000 per lot.

▶️ Read the full case

Brochot, S. (2021). Metal accounting: a direct link between sampling and financial management. Spectroscopy Europe, vol. 33, no. 7.

What is AMIRA P754 and why does it matter?

AMIRA P754 is the Code of Practice and Guidelines for Metallurgical Accounting published by AMIRA Global. It defines 10 principles covering accurate measurement, transparent calculation rules, data validation and reconciliation, governance structures, and routine audits.

P754 matters because it simultaneously satisfies the production data requirements of SOX, NI 43-101, JORC, SAMREC, and GISTM. Stock exchanges increasingly reference it as the production reporting standard.

▶️ This article could interest you

Metal accounting AMIRA code P754 principles

What is data reconciliation in metallurgical accounting?

Data reconciliation is the statistical process of adjusting measured values so they satisfy mass conservation laws while remaining as close as possible to original measurements. It uses a least-squares adjustment weighted by each measurement’s uncertainty.

The result is a coherent metal balance with quantified confidence intervals on each stream. Meaningful reconciliation requires correctly calculated measurement uncertainties at every point in the sampling chain (Brochot, 2015, TOS Forum, DOI: 10.1255/tosf.73). CASPEO implements data reconciliation using INVENTEO software, integrated with sampling uncertainty calculations from ECHANT.

What does a metal accounting audit include?

A metal accounting audit evaluates five domains: sampling and mass measurement, data integrity and validation, mass balance and reconciliation methods, governance and documentation, and reporting and compliance alignment with AMIRA P754.

The audit uses the overall measurement error framework (OE = Total Sampling Error + Analytical Error) to quantify uncertainty at each point in the data chain, then traces that uncertainty through to the reconciled metal balance.

▶️ This article could interest you

Brochot, S. (2021). Metal accounting: a direct link between sampling and financial management. Spectroscopy Europe, vol. 33, no. 7.

How to achieve AMIRA P754 compliance?

AMIRA P754 compliance requires aligning measurement systems, calculation methods, documentation, and governance with the 10 P754 principles. Compliance is not achieved through software alone. It requires disciplined measurement practices, documented methodologies, and ongoing review.

CASPEO’s six-step methodology: (1) gap analysis, (2) measurement framework definition, (3) transparent calculation rules, (4) data validation and reconciliation, (5) governance and audit structure, (6) system implementation with INVENTEO.

AMIRA P754 compliance is not achieved through software alone. It requires disciplined measurement practices, documented methodologies, and ongoing review to maintain transparency and reliability over time.

▶️ This article could interest you

How INVENTEO can help you implement a metal accounting system compliant with AMIRA P75

Can spreadsheets meet AMIRA P754 requirements?

Spreadsheets cannot meet AMIRA P754 requirements for operations of significant complexity. P754 Principle 3 requires immutable audit trails (spreadsheets can be overwritten without trace), Principle 4 requires competent person controls (unenforceable in shared spreadsheets), and Principle 5 requires automated data validation.

Purpose-built software such as INVENTEO automates reconciliation, reduces manual effort, and provides shift-to-shift visibility that spreadsheets cannot match.

▶️ This article could interest you

Brochot, S. & Durance, M.-V. (2012). A New Approach to Metallurgical Accounting. 11th Mill Operators’ Conference, Hobart, Australia, pp. 217-223.

Is metal accounting only for large companies?

There’s a common misconception that rigorous metallurgical accounting is only for large, publicly-listed mining companies.

The reality? Every operation tracking metal value needs reliable metal accounting. The complexity and formality scale with your operation, but the principles don’t change: accurate measurement, proper reconciliation, and documented procedures.

Relying on Excel or manual spreadsheets may seem sufficient at first, but these tools quickly reach their limits: version control becomes difficult, formulas can be hidden or copied incorrectly, and audit trails disappear.

Why audit a metallurgical accounting system?

An audit is required when any component — measurement, reconciliation, data management, or governance — may be producing unreliable results. Operations typically request an audit when metal balances won’t close, mine-mill reconciliation shows discrepancies, laboratory data is inconsistent, or reporting requirements have changed.

With converging regulatory frameworks, a weakness in one component creates simultaneous gaps across SOX, NI 43-101, JORC, SAMREC, and GISTM.

CASPEO live

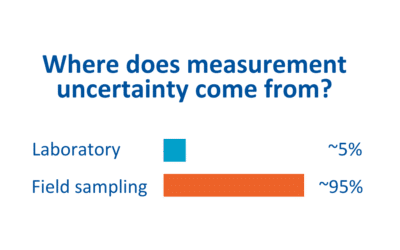

Where do sampling errors come from in mineral processing? Sampling errors field vs laboratory uncertainty

In mineral processing operations, the largest source of measurement uncertainty is field sampling, not the laboratory. CASPEO's audits of mining operations across 70 countries show a consistent...

INVENTEO metal accounting software update: discover the 2025 new features

CASPEO is proud to unveil major new features for its INVENTEO metal accounting software. Discover the 2025 version.Implement a compliant metal accounting system aligned with your operational...

Society for Mining, Metallurgy & Exploration: short course on metal accounting in 2023

CASPEO will be part of a panel of mining industry experts presenting a short course on metal accounting at the annual meeting of the the Society for Mining, Metallurgy & Exploration (SME) Nevada...

Subscribe to our newsletter

Ready to transform your system with CASPEO’s metal accounting consulting services

Contact us to discuss your metallurgical accounting challenges and explore solutions appropriate for your operation.

CASPEO provides process simulation software, metallurgical accounting solutions, and expert consulting for the mining and metallurgy industries worldwide. Through our integrated approach that combines statistical data analysis, advanced process modeling, and mass balance reconciliation, we help you build the data-quality backbone to improve efficiency, strength sustainability, consolidate governance, and succeed in your digital transformation. With CASPEO, go beyond process simulation.

Stay tuned!

Empower your decisions

Consulting

Engineering software

Get a quote

Develop your skills

Courses

Blog

Get a live demo

Need assistance?

Online support

Contact us

Site map

2026 © CASPEO - All rights reserved